SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE TO

Tender Offer Statement Under Section

14(d)(1) or 13(e)(1)

of the Securities Exchange Act of 1934

Merus N.V.

(Name of Subject Company)

Genmab Holding II B.V.

and

Genmab A/S

(Name of Filing Persons (Offerors))

Common Share, nominal value €0.09 per share

(Title of Class of Securities)

N5749R100

(CUSIP Number of Class of Securities)

Greg Mueller

Carl Jacobsens Vej 30

2500 Valby

Denmark

+45 70 20 27 28

(Name, Address and Telephone Number of Person Authorized

to Receive Notices and Communications on Behalf of Filing Persons)

Copy to:

Clare O’Brien

Derrick Lott

Harald Halbhuber

Allen Overy Shearman Sterling US LLP

599 Lexington Avenue

New York, NY 10022

Telephone: +1 (212) 848-4000

Calculation of Filing Fee

| Transaction Valuation | Amount of Filing Fee |

| N/A | N/A |

| ☐ | Check the box if any part of the fee is offset as provided by Rule 0-11(a)(2) and identify the filing with which the offsetting fee was previously paid. Identify the previous filing by registration statement number, or the Form or Schedule and date of its filing. |

| Amount Previously Paid: N/A | Filing Party: N/A |

| Form or Registration No.: N/A | Date Filed: N/A |

| ☒ | Check the box if the filing relates solely to preliminary communications made before the commencement of a tender offer. |

Check the appropriate boxes below to designate any transactions to which the statement relates:

| ☒ | third-party tender offer subject to Rule 14d-1. |

| ☐ | issuer tender offer subject to Rule 13e-4. |

| ☐ | going-private transaction subject to Rule 13e-3. |

| ☐ | amendment to Schedule 13D under Rule 13d-2. |

Check the following box if the filing is a final amendment reporting the results of the tender offer: ☐

SCHEDULE TO

The pre-commencement communications filed under cover of this Tender Offer Statement on Schedule TO are being filed by Genmab A/S, a public limited liability company incorporated in Denmark (“Genmab”), pursuant to General Instruction D to Schedule TO related to a planned cash tender offer for all of the issued and outstanding common shares, nominal value €0.09 per share of Merus N.V., a public limited liability company (naamloze vennootschap) organized under the Laws of The Netherlands (the “Company”) pursuant to the Transaction Agreement, dated as of September 29, 2025, by and among Genmab, Genmab Holding II B.V., a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid) organized under the Laws of the Netherlands and a wholly-owned subsidiary of Genmab (“Purchaser”), and the Company.

Additional Information

The tender offer for the common shares of the Company (“Common Shares”) referenced in this announcement has not yet commenced. This announcement is for informational purposes only and is neither an offer to purchase nor a solicitation of an offer to sell Common Shares or any other securities, nor is it a substitute for the tender offer materials that Genmab and Purchaser will file or cause to be filed with the Securities and Exchange Commission (the “SEC”) upon the commencement of the tender offer. This communication may be deemed to be solicitation material in respect of the EGM Proposals (defined below). At the time the tender offer is commenced, Genmab and Purchaser will file or cause to be filed with the SEC a tender offer statement on Schedule TO (the “Tender Offer Statement”), and the Company will file with the SEC a solicitation/recommendation statement on Schedule 14D-9 (the “Solicitation/Recommendation Statement”), in each case, with respect to the tender offer. The Company also intends to file with the SEC a proxy statement on Schedule 14A in connection with an extraordinary general meeting of the Company’s shareholders, at which the Company’s shareholders will vote on certain proposed resolutions (the “EGM Proposals”) in connection with the transactions referenced herein, and will mail the definitive proxy statement and a proxy card to each shareholder of the Company entitled to vote at the extraordinary general meeting. THE TENDER OFFER STATEMENT (INCLUDING AN OFFER TO PURCHASE, A RELATED LETTER OF TRANSMITTAL AND CERTAIN OTHER TENDER OFFER DOCUMENTS), THE SOLICITATION/RECOMMENDATION STATEMENT AND THE PROXY STATEMENT WILL CONTAIN IMPORTANT INFORMATION. SHAREHOLDERS OF THE COMPANY ARE URGED TO READ THESE DOCUMENTS CAREFULLY WHEN THEY BECOME AVAILABLE (AS EACH MAY BE AMENDED OR SUPPLEMENTED FROM TIME TO TIME) BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION THAT HOLDERS OF COMMON SHARES SHOULD CONSIDER BEFORE MAKING ANY DECISION WITH RESPECT TO THE TENDER OFFER OR MAKING ANY VOTING DECISION. The tender offer for Common Shares will be made only pursuant to the Offer to Purchase, the Letter of Transmittal and related documents filed as a part of the Tender Offer Statement. The Tender Offer Statement (including the Offer to Purchase, the related Letter of Transmittal and certain other tender offer documents), as well as the Solicitation/Recommendation Statement, will be made available to all holders of Common Shares at no expense to them. The Tender Offer Statement and the Solicitation/Recommendation Statement will be made available for free at the SEC’s website at www.sec.gov. Copies of the documents filed by Genmab or Purchaser with the SEC will also be available free of charge on Parent’s website at https://www.genmab.com/investor-relations or by contacting Genmab’s investor relations department at ir@genmab.com. Copies of the documents filed by the Company with the SEC will also be available free of charge on the Company’s website at https://ir.merus.nl/ or by contacting the Company’s investor relations department at s.spear@merus.nl. In addition, shareholders of the Company may obtain free copies of the tender offer materials by contacting the information agent for the tender offer that will be named in the Tender Offer Statement.

Forward-looking Statements

This Company Announcement contains forward looking statements. The words “believe,” “expect,” “anticipate,” “intend” and “plan” and similar expressions identify forward looking statements. Statements in this Company Announcement that are forward looking may include, but are not limited to, statements regarding the benefits of the proposed transaction; the development plan, regulatory approval, data release timing, commercial launch timing and revenue potential of petosemtamab; the expected timing of the closing of the proposed transaction; and Genmab’s expectations regarding financing the proposed transaction, de-levering and timing of new drug launches. Actual results or performance may differ materially from any future results or performance expressed or implied by such statements. The important factors that could cause our actual results or performance to differ materially include, among others, the occurrence of any event, change or other circumstance that could give rise to the right of Genmab or the Company or both of them to terminate the transaction agreement, including circumstances requiring a party to pay the other party a termination fee pursuant to the transaction agreement; the failure to obtain applicable regulatory approvals or clearances or the Company shareholder approval in a timely manner or otherwise; the risk that the proposed transaction may not close in the anticipated timeframe or at all due to one or more of the other closing conditions to the proposed transaction not being satisfied or waived; the risk that there may be unexpected costs, charges or expenses resulting from the proposed transaction; risks related to the ability of Genmab to successfully integrate the Company’s business with Genmab’s existing businesses and achieve the expected benefits of the proposed transaction within the expected timeframes or at all and the possibility that such integration may be more difficult, time consuming or costly than expected; risks that the proposed transaction disrupts Genmab’s or the Company’s current plans and operations; risks related to disruption of each company’s management’s time and attention from ongoing business operations due to the proposed transaction; continued availability of capital and financing and rating agency actions; the risk that any announcements relating to the proposed transaction could have adverse effects on the market price of Genmab’s and/or the Company’s securities or operating results; the risk that the proposed transaction and its announcement could have an adverse effect on the ability of Genmab and the Company to retain and hire key personnel, and to maintain relationships with their respective business partners and on their respective operating results and businesses generally; risks typically associated with conducting clinical trials, including the risk that additional clinical trials testing the Company’s products may not be successful; the risk that the Company’s products may not be approved on expected timelines or at all; the risk of litigation that could be instituted against Genmab or its directors, managers or officers and/or regulatory actions related to the proposed transaction, including the effects of any outcomes related thereto; risks related to unpredictable and severe or catastrophic events, including but not limited to acts of terrorism, war or hostilities, cyber-attacks, or the impact of any pandemic, epidemic or outbreak of an infectious disease in the United States or worldwide on Genmab’s and/or the Company’s business, financial condition and results of operations, as well the response thereto by each company’s management; and other business effects, including the effects of industry, market, economic, political or regulatory conditions. Also, actual results or performance of Genmab and the Company may differ materially from any future results or performance expressed or implied by such statements for a number of additional reasons as described in Genmab’s and the Company’s respective filings with the SEC, including those included in Genmab’s most recent Annual Report on Form 20-F, which is available at www.genmab.com and www.sec.gov and those included in the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2025, which is available at https://ir.merus.nl/ and www.sec.gov. Neither Genmab nor the Company undertakes any obligation to update or revise forward looking statements in this Company Announcement nor to confirm such statements to reflect subsequent events or circumstances after the date made or in relation to actual results, unless required by law.

***

| Item 12. | Exhibits. |

| (a)(5)(a) | Company Announcement, dated September 29, 2025: Genmab to Acquire Merus, Expanding Late-Stage Pipeline and Accelerating into a Wholly Owned Model |

| (a)(5)(b) | Genmab investor call slides, dated September 29, 2025 |

| (a)(5)(c) | Social Media posts of Genmab and Jan G.J. van de Winkel, President and Chief Executive Officer of Genmab, dated September 29, 2025 |

| (a)(5)(d) | Investor Relations call transcript, dated September 29, 2025 |

Genmab to Acquire Merus, Expanding Late-Stage Pipeline and Accelerating into a Wholly Owned Model

Company Announcement

- Genmab to acquire Merus for USD 97.00 per share in an all-cash transaction representing a transaction value of approximately USD 8.0 billion

- Proposed acquisition adds petosemtamab, a late-stage asset with two Breakthrough Therapy Designations, to Genmab’s portfolio

- Transaction anticipated to be accretive to EBITDA by end of 2029

- Genmab to host a conference call today at 1:00 PM CEST / 12:00 PM BST / 7:00 AM EDT

COPENHAGEN, Denmark; UTRECHT, The Netherlands; September 29, 2025, – Genmab A/S (Nasdaq: GMAB) and Merus N.V. (Nasdaq: MRUS) announced today that they have entered into a transaction agreement pursuant to which Genmab intends to acquire all the shares of Merus, a clinical-stage biotechnology company with its late-stage breakthrough therapy asset petosemtamab, which is in Phase 3 development, for USD 97.00 per share in an all-cash transaction representing a transaction value of approximately USD 8.0 billion. The transaction has been unanimously approved by the Boards of Directors of both companies. A wholly owned subsidiary of Genmab (“Purchaser”) will commence a tender offer for 100% of Merus’ common shares, which is anticipated to close by early in the first quarter of 2026.

The proposed acquisition of Merus is expected to meaningfully accelerate Genmab’s shift to a wholly owned model, expanding and diversifying the company’s revenue, driving sustained growth into the next decade and contributing to Genmab’s evolution into a biotechnology leader. The addition of petosemtamab, Merus’ lead asset, to Genmab’s promising late-stage pipeline is a compelling strategic fit with Genmab’s portfolio and aligns with Genmab’s expertise in antibody therapy development and commercialization in oncology. Following the closing of the transaction, Genmab will have four proprietary programs expected to drive multiple new drug launches by 2027.

“The proposed acquisition of Merus clearly aligns with our long-term strategy. It has the potential to significantly accelerate our evolution into a global biotechnology leader by providing durable growth for the company well into the next decade,” said Jan van de Winkel, Ph.D., President and Chief Executive Officer of Genmab. “Petosemtamab has the potential to be a transformational therapy for patients living with head and neck cancer. With our proven track record of success, both in clinical development and in commercialization, we are confident that we will be able to unlock the promise of petosemtamab.”

“We are excited for the opportunity to join Genmab, a leader in antibody therapeutics, to further develop and bring petosemtamab to patients. Our two companies have a rich history of innovation with multiple approvals in the field of multispecific antibodies. We believe Genmab has the right vision and experience to advance petosemtamab in recurrent/metastatic head and neck cancer and beyond,” said Bill Lundberg, M.D., President, Chief Executive Officer of Merus. “I’m immensely proud of the Merus team who have pioneered our foundational platform technologies to make better medicines and who have demonstrated - with an approved product and a product candidate, petosemtamab, in registrational studies - an ability to deliver on our promise to close in on cancer.”

Petosemtamab is an EGFRxLGR5 bispecific antibody

with the potential to be both first- and best-in-class in head and neck cancer. It has been granted two Breakthrough Therapy Designations

(BTD) by the U.S. Food and Drug Administration (FDA) for first- and second-line plus head and neck cancer indications. Of note, compelling

Phase 2 data was presented at the American Society for Clinical Oncology (ASCO) 2025 Annual Meeting showing both an overall response rate

and median progression free survival that were substantially higher than standard of care.

Genmab A/S Carl Jacobsens Vej 30 2500 Valby, Denmark | Tel: +45 7020 2728 www.genmab.com | Company Announcement no. 46 Page 1/5 CVR no. 2102 3884 LEI Code 529900MTJPDPE4MHJ122 |

Genmab to Acquire Merus, Expanding Late-Stage Pipeline and Accelerating into a Wholly Owned Model

Merus is currently running two Phase 3 trials in first- and second/third line head and neck cancer, with topline interim readout of one or both trials anticipated in 2026. Based on Genmab’s experience in late-stage development and excellence in commercial execution, Genmab anticipates the potential for the initial launch of petosemtamab in 2027, subject to clinical results and regulatory approvals. Genmab also intends to broaden and accelerate petosemtamab’s development with potential expansion into earlier lines of therapy. Following its initial anticipated approval, Genmab believes that petosemtamab will be accretive to EBITDA with at least one-billion-dollar annual sales potential by 2029, with multi-billion-dollar annual revenue potential thereafter.

Details of the Transaction and Financing

Under the transaction agreement, Purchaser, a wholly owned subsidiary of Genmab, will commence a tender offer for all the outstanding common shares of Merus. Following the closing of the tender offer, Merus and Genmab will effect a series of transactions resulting in Genmab owning 100% of the common shares of Merus (or a successor entity). Depending on the structure of the back end transactions, Merus shareholders that do not tender their shares into the tender offer will either receive the same consideration for their common shares as the common shares tendered into the tender offer (subject to applicable withholding taxes) or a fair price for their common shares determined by a Dutch court in statutory buy-out proceedings. The closing of the tender offer is subject to the satisfaction of customary closing conditions for similar transactions, including a minimum acceptance condition of at least 80% of Merus’ common shares (which threshold may be reduced to 75% unilaterally by Genmab if all other closing conditions are satisfied), approval by Merus’ shareholders of resolutions relating to Merus’ post-closing governance and the back end transactions at Merus’ extraordinary shareholders meeting to be held for that purpose, and completion of the relevant works councils consultation processes.

The USD 97.00 per common share purchase price payable in the tender offer represents a premium of approximately 41% over Merus’ closing stock price on September 26, 2025, of USD 68.89 and approximately 44% over Merus’ 30-day volume weighted average price of USD 67.42.

The transaction is not subject to a financing condition. Consideration is expected to be funded through a combination of cash on hand and approximately $5.5 billion of non-convertible debt financing. Genmab has obtained a funding commitment from Morgan Stanley Senior Funding, Inc. for this amount.

The financing package includes a meaningful portion of prepayable debt, in line with Genmab’s commitment to deleveraging with a target of gross leverage <3x within two years after the closing of the proposed transaction. Today’s news does not impact Genmab’s financial guidance for the full year 2025, last issued on August 7, 2025. Genmab will provide its financial outlook for the full year 2026 in conjunction with its full year 2025 earnings report in February 2026.

PJT Partners and Morgan Stanley & Co. International plc are acting as joint financial advisors to Genmab and A&O Shearman and Kromann Reumert as its legal advisors.

Jefferies LLC is acting as financial advisor to Merus and Latham & Watkins and NautaDutilh as its legal advisors.

Conference Call Details

Genmab will hold a conference call to discuss the transaction today, September 29, 2025 at 1:00 PM CEST / 12:00 PM BST / 7:00 AM EDT.

To join the call please use the following registration link https://register-conf.media-server.com/register/BI65be2c038b9b42dbb064dfc843b6a478.

Registered participants will receive an email with a link to access dial-in information as well as a unique personal PIN. A live and

archived webcast of the calls and relevant slides will be available at https://www.genmab.com/investor-relations.

Genmab A/S Carl Jacobsens Vej 30 2500 Valby, Denmark | Tel: +45 7020 2728 www.genmab.com | Company Announcement no. 46 Page 2/5 CVR no. 2102 3884 LEI Code 529900MTJPDPE4MHJ122 |

Genmab to Acquire Merus, Expanding Late-Stage Pipeline and Accelerating into a Wholly Owned Model

About Genmab

Genmab is an international biotechnology company with a core purpose of guiding its unstoppable team

to strive toward improving the lives of patients with innovative and differentiated antibody therapeutics. For more than 25 years, its

passionate, innovative and collaborative team has invented next-generation antibody technology platforms and leveraged translational,

quantitative and data sciences, resulting in a proprietary pipeline including bispecific T-cell engagers, antibody-drug conjugates, next-generation

immune checkpoint modulators and effector function-enhanced antibodies. By 2030, Genmab’s vision is to transform the lives of people

with cancer and other serious diseases with knock-your-socks-off (KYSO) antibody medicines®.

Established in 1999, Genmab is headquartered in Copenhagen, Denmark, with international presence across North America, Europe and Asia Pacific. For more information, please visit Genmab.com and follow us on LinkedIn and X.

About Merus

Merus is an oncology company developing innovative full-length human bispecific and trispecific antibody therapeutics, referred to as Multiclonics®. Multiclonics® are manufactured using industry standard processes and have been observed in preclinical and clinical studies to have several of the same features of conventional human monoclonal antibodies, such as long half-life and low immunogenicity. For additional information, please visit Merus’ website, LinkedIn and Bluesky.

Additional Information

The tender offer for the common shares (“Common Shares”) of Merus referenced in this announcement has not yet commenced. This announcement is for informational purposes only and is neither an offer to purchase nor a solicitation of an offer to sell Common Shares or any other securities, nor is it a substitute for the tender offer materials that Genmab and Purchaser will file or cause to be filed with the Securities and Exchange Commission (the “SEC”) upon the commencement of the tender offer. This communication may be deemed to be solicitation material in respect of the EGM Proposals (defined below). At the time the tender offer is commenced, Genmab and Purchaser will file or cause to be filed with the SEC a tender offer statement on Schedule TO (the “Tender Offer Statement”), and Merus will file with the SEC a solicitation/recommendation statement on Schedule 14D-9 (the “Solicitation/Recommendation Statement”), in each case, with respect to the tender offer. Merus also intends to file with the SEC a proxy statement on Schedule 14A in connection with an extraordinary general meeting of Merus’ shareholders, at which Merus’ shareholders will vote on certain proposed resolutions (the “EGM Proposals”) in connection with the transactions referenced herein, and will mail the definitive proxy statement and a proxy card to each shareholder of Merus entitled to vote at the extraordinary general meeting. THE TENDER OFFER STATEMENT (INCLUDING AN OFFER TO PURCHASE, A RELATED LETTER OF TRANSMITTAL AND CERTAIN OTHER TENDER OFFER DOCUMENTS), THE SOLICITATION/RECOMMENDATION STATEMENT AND THE PROXY STATEMENT WILL CONTAIN IMPORTANT INFORMATION. SHAREHOLDERS OF MERUS ARE URGED TO READ THESE DOCUMENTS CAREFULLY WHEN THEY BECOME AVAILABLE (AS EACH MAY BE AMENDED OR SUPPLEMENTED FROM TIME TO TIME) BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION THAT HOLDERS OF COMMON SHARES SHOULD CONSIDER BEFORE MAKING ANY DECISION WITH RESPECT TO THE TENDER OFFER OR MAKING ANY VOTING DECISION. The tender offer for Common Shares will be made only pursuant to the Offer to Purchase, the Letter of Transmittal and related documents filed as a part of the Tender Offer Statement. The Tender Offer Statement (including the Offer to Purchase, the related Letter of Transmittal and certain other tender offer documents), as well as the Solicitation/Recommendation Statement, will be made available to all holders of Common Shares at no expense to them. The Tender Offer Statement and the Solicitation/Recommendation Statement will be made available for free at the SEC’s website at www.sec.gov. Copies of the documents filed by Genmab or Purchaser with the SEC will also be available free of charge on Genmab’s website at https://www.genmab.com/investor-relations or by contacting Genmab’s investor relations department at ir@genmab.com. Copies of the documents filed by Merus with the SEC will also be available free of charge on Merus’ website at https://ir.merus.nl/ or by contacting Merus’ investor relations department at s.spear@merus.nl. In addition, shareholders of Merus may obtain free copies of the tender offer materials by contacting the information agent for the tender offer that will be named in the Tender Offer Statement.

Genmab A/S Carl Jacobsens Vej 30 2500 Valby, Denmark | Tel: +45 7020 2728 www.genmab.com | Company Announcement no. 46 Page 3/5 CVR no. 2102 3884 LEI Code 529900MTJPDPE4MHJ122 |

Genmab to Acquire Merus, Expanding Late-Stage Pipeline and Accelerating into a Wholly Owned Model

Participants in the Solicitation

Merus and certain of its directors, executive officers and other members of management and employees may be deemed to be participants in soliciting proxies from its shareholders in connection with the proposed back end transactions. Information regarding the persons who may, under the rules of the SEC, be considered to be participants in the solicitation of Merus’ shareholders in connection with the proposed back end transactions will be set forth in Merus’ definitive proxy statement for its extraordinary general meeting at which the EGM Proposals will be submitted for approval by Merus’ shareholders. You may also find additional information about Merus’ directors and executive officers in Merus’ Annual Report on Form 10-K for the year ended December 31, 2024, which was filed with the SEC on February 27, 2025 (as amended) and Merus’ Definitive Proxy Statement for its 2025 annual general meeting of shareholders, which was filed with the SEC on April 24, 2025.

Genmab Contacts:

Marisol Peron, Senior Vice President, Global Communications & Corporate Affairs

T: +1 609 524 0065; E: mmp@genmab.com

Andrew Carlsen, Vice President, Head of Investor Relations

T: +45 3377 9558; E: acn@genmab.com

Merus Contacts:

Sherri Spear, Senior Vice President, Investor Relations and Strategic Communications

T: 617-821-3246; E: s.spear@merus.nl

Kathleen Farren, Director Investor Relations and Corporate Communications

T: 617-230-4165; E: k.farren@merus.nl

Genmab A/S Carl Jacobsens Vej 30 2500 Valby, Denmark | Tel: +45 7020 2728 www.genmab.com | Company Announcement no. 46 Page 4/5 CVR no. 2102 3884 LEI Code 529900MTJPDPE4MHJ122 |

Genmab to Acquire Merus, Expanding Late-Stage Pipeline and Accelerating into a Wholly Owned Model

This Company Announcement contains forward looking statements. The words “believe,” “expect,” “anticipate,” “intend” and “plan” and similar expressions identify forward looking statements. Statements in this Company Announcement that are forward looking may include, but are not limited to, statements regarding: the benefits and potential effects of the proposed transaction; the development plan, regulatory approval, data release timing, commercial launch timing and revenue potential of petosemtamab; the expected timing of the closing of the proposed transaction; and Genmab’s expectations regarding financing the proposed transaction, de-levering and timing of new drug launches. Actual results or performance may differ materially from any future results or performance expressed or implied by such statements. The important factors that could cause our actual results or performance to differ materially include, among others, the occurrence of any event, change or other circumstance that could give rise to the right of Genmab or Merus or both of them to terminate the transaction agreement, including circumstances requiring a party to pay the other party a termination fee pursuant to the transaction agreement; the failure to obtain applicable regulatory approvals or clearances or Merus shareholder approval in a timely manner or otherwise; the risk that the proposed transaction may not close in the anticipated timeframe or at all due to one or more of the other closing conditions to the proposed transaction not being satisfied or waived; the risk that there may be unexpected costs, charges or expenses resulting from the proposed transaction; risks related to the ability of Genmab to successfully integrate Merus’ business with Genmab’s existing businesses and achieve the expected benefits of the proposed transaction within the expected timeframes or at all and the possibility that such integration may be more difficult, time consuming or costly than expected; risks that the proposed transaction disrupts Genmab’s or Merus’ current plans and operations; risks related to disruption of each company’s management’s time and attention from ongoing business operations due to the proposed transaction; continued availability of capital and financing and rating agency actions; the risk that any announcements relating to the proposed transaction could have adverse effects on the market price of Genmab’s and/or Merus’ securities or operating results; the risk that the proposed transaction and its announcement could have an adverse effect on the ability of Genmab and Merus to retain and hire key personnel, and to maintain relationships with their respective business partners and on their respective operating results and businesses generally; risks typically associated with conducting clinical trials, including the risk that additional clinical trials testing Merus’ products may not be successful; the risk that Merus’ products may not be approved on expected timelines or at all; the risk of litigation that could be instituted against Genmab or its directors, managers or officers and/or regulatory actions related to the proposed transaction, including the effects of any outcomes related thereto; risks related to unpredictable and severe or catastrophic events, including but not limited to acts of terrorism, war or hostilities, cyber-attacks, or the impact of any pandemic, epidemic or outbreak of an infectious disease in the United States or worldwide on Genmab’s and/or Merus’ business, financial condition and results of operations, as well the response thereto by each company’s management; and other business effects, including the effects of industry, market, economic, political or regulatory conditions. Also, actual results or performance of Genmab and Merus may differ materially from any future results or performance expressed or implied by such statements for a number of additional reasons as described in Genmab’s and Merus’ respective filings with the SEC, including those included in Genmab’s most recent Annual Report on Form 20-F, which is available at www.genmab.com and www.sec.gov, and those included in Merus’ Quarterly Report on Form 10-Q for the quarter ended June 30, 2025, which is available at https://merus.nl/ and www.sec.gov. Neither Genmab nor Merus undertakes any obligation to update or revise forward looking statements in this Company Announcement nor to confirm such statements to reflect subsequent events or circumstances after the date made or in relation to actual results, unless required by law.

Genmab A/S and/or its subsidiaries own the following trademarks: Genmab®; the Y-shaped Genmab logo®; Genmab

in combination with the Y-shaped Genmab logo®; HuMax®; DuoBody®; HexaBody®;

DuoHexaBody®, HexElect® and KYSO®.

Multiclonics®, Biclonics®, Triclonics® and ADClonics® are registered trademarks of Merus N.V.

Genmab A/S Carl Jacobsens Vej 30 2500 Valby, Denmark | Tel: +45 7020 2728 www.genmab.com | Company Announcement no. 46 Page 5/5 CVR no. 2102 3884 LEI Code 529900MTJPDPE4MHJ122 |

Genmab Delivering Genmab's Next Decade of Sustainable Growth Genmab to Acquire Merus (c) Genmab 2025

Forward Looking Statement This Company Announcement contains forward looking statements. The words "believe," "expect," "anticipate," "intend" and "plan" and similar expressions identify forward looking statements. Statements in this Company Announcement that are forward looking may include, but are not limited to, statements regarding the benefits of the proposed transaction; the development plan, regulatory approval, data release timing, commercial launch timing and revenue potential of petosemtamab; the expected timing of the closing of the proposed transaction; and Genmab's expectations regarding financing the proposed transaction, de-levering and timing of new drug launches. Actual results or performance may differ materially from any future results or performance expressed or implied by such statements. The important factors that could cause our actual results or performance to differ materially include, among others, the occurrence of any event, change or other circumstance that could give rise to the right of Genmab or Merus or both of them to terminate the transaction agreement, including circumstances requiring a party to pay the other party a termination fee pursuant to the transaction agreement; the failure to obtain applicable regulatory approvals or clearances or Merus shareholder approval in a timely manner or otherwise; the risk that the proposed transaction may not close in the anticipated timeframe or at all due to one or more of the other closing conditions to the proposed transaction not being satisfied or waived; the risk that there may be unexpected costs, charges or expenses resulting from the proposed transaction; risks related to the ability of Genmab to successfully integrate Merus' business with Genmab's existing businesses and achieve the expected benefits of the proposed transaction within the expected timeframes or at all and the possibility that such integration may be more difficult, time consuming or costly than expected; risks that the proposed transaction disrupts Genmab's or Merus' current plans and operations; risks related to disruption of each company's management's time and attention from ongoing business operations due to the proposed transaction; continued availability of capital and financing and rating agency actions; the risk that any announcements relating to the proposed transaction could have adverse effects on the market price of Genmab's and/or Merus' securities or operating results; the risk that the proposed transaction and its announcement could have an adverse effect on the ability of Genmab and Merus to retain and hire key personnel, and to maintain relationships with their respective business partners and on their respective operating results and businesses generally; risks typically associated with conducting clinical trials, including the risk that additional clinical trials testing Merus' products may not be successful; the risk that Merus' products may not be approved on expected timelines or at all; the risk of litigation that could be instituted against Genmab or its directors, managers or officers and/or regulatory actions related to the proposed transaction, including the effects of any outcomes related thereto; risks related to unpredictable and severe or catastrophic events, including but not limited to acts of terrorism, war or hostilities, cyber-attacks, or the impact of any pandemic, epidemic or outbreak of an infectious disease in the United States or worldwide on Genmab's and/or Merus' business, financial condition and results of operations, as well the response thereto by each company's management; and other business effects, including the effects of industry, market, economic, political or regulatory conditions. Also, actual results or performance of Genmab and Merus may differ materially from any future results or performance expressed or implied by such statements for a number of additional reasons as described in Genmab's and Merus' respective filings with the Securities and Exchange Commission (the "SEC"), including those included in Genmab's most recent Annual Report on Form 20-F, which is available at www.genmab.com and www.sec.gov and those included in Merus' most recent Quarterly Report on Form 10-Q for the quarter ended June 30, 2025, which is available at https://merus.nl/ and www.sec.gov. Neither Genmab nor Merus undertakes any obligation to update or revise forward looking statements in this Company Announcement nor to confirm such statements to reflect subsequent events or circumstances after the date made or in relation to actual results, unless required by law. Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 2

Additional Information The tender offer for the common shares ("Common Shares") of Merus referenced in this announcement has not yet commenced. This announcement is for informational purposes only and is neither an offer to purchase nor a solicitation of an offer to sell Common Shares or any other securities, nor is it a substitute for the tender offer materials that Genmab and Purchaser will file or cause to be filed with the SEC upon the commencement of the tender offer. This communication may be deemed to be solicitation material in respect of the EGM Proposals (defined below). At the time the tender offer is commenced, Genmab and a wholly owned subsidiary of Genmab ("Purchaser") will file or cause to be filed with the SEC a tender offer statement on Schedule TO (the "Tender Offer Statement"), and Merus will file with the SEC a solicitation/recommendation statement on Schedule 14D-9 (the "Solicitation/Recommendation Statement"), in each case, with respect to the tender offer. Merus also intends to file with the SEC a proxy statement on Schedule 14A in connection with an extraordinary general meeting of Merus' shareholders, at which Merus' shareholders will vote on certain proposed resolutions (the "EGM Proposals") in connection with the transactions referenced herein, and will mail the definitive proxy statement and a proxy card to each shareholder of Merus entitled to vote at the extraordinary general meeting. THE TENDER OFFER STATEMENT (INCLUDING AN OFFER TO PURCHASE, A RELATED LETTER OF TRANSMITTAL AND CERTAIN OTHER TENDER OFFER DOCUMENTS), THE SOLICITATION/RECOMMENDATION STATEMENT AND THE PROXY STATEMENT WILL CONTAIN IMPORTANT INFORMATION. SHAREHOLDERS OF MERUS ARE URGED TO READ THESE DOCUMENTS CAREFULLY WHEN THEY BECOME AVAILABLE (AS EACH MAY BE AMENDED OR SUPPLEMENTED FROM TIME TO TIME) BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION THAT HOLDERS OF COMMON SHARES SHOULD CONSIDER BEFORE MAKING ANY DECISION WITH RESPECT TO THE TENDER OFFER OR MAKING ANY VOTING DECISION. The tender offer for Common Shares will be made only pursuant to the Offer to Purchase, the Letter of Transmittal and related documents filed as a part of the Tender Offer Statement. The Tender Offer Statement (including the Offer to Purchase, the related Letter of Transmittal and certain other tender offer documents), as well as the Solicitation/Recommendation Statement, will be made available to all holders of Common Shares at no expense to them. The Tender Offer Statement and the Solicitation/Recommendation Statement will be made available for free at the SEC's website at www.sec.gov. Copies of the documents filed by Genmab or Purchaser with the SEC will also be available free of charge on Genmab's website at https://www.genmab.com/investor-relations or by contacting Genmab's investor relations department at ir@genmab.com. Copies of the documents filed by Merus with the SEC will also be available free of charge on Merus' website at https://ir.merus.nl/ or by contacting Merus' investor relations department at s.spear@merus.nl. In addition, shareholders of Merus may obtain free copies of the tender offer materials by contacting the information agent for the tender offer that will be named in the Tender Offer Statement. Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 3

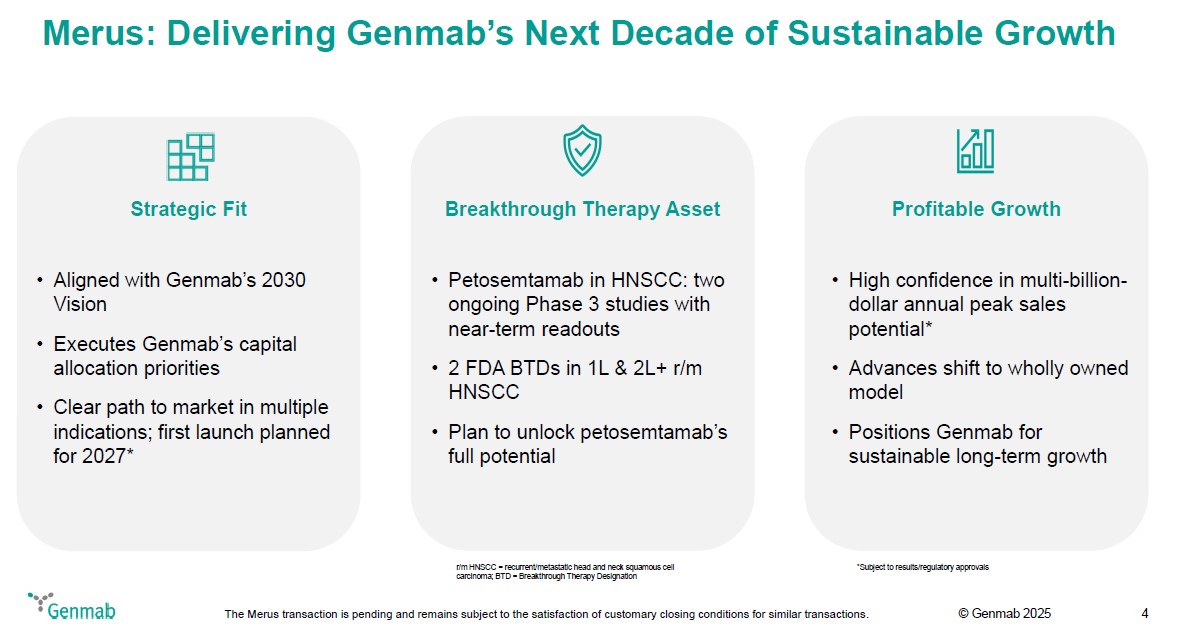

Merus: Delivering Genmab's Next Decade of Sustainable Growth Strategic Fit Aligned with Genmab's 2030 Vision Executes Genmab's capital allocation priorities Clear path to market in multiple indications; first launch planned for 2027* Breakthrough Therapy Asset Petosemtamab in HNSCC: two ongoing Phase 3 studies with near-term readouts 2 FDA BTDs in 1L & 2L+ r/m HNSCC Plan to unlock petosemtamab's full potential r/m HNSCC = recurrent/metastatic head and neck squamous cell carcinoma; BTD = Breakthrough Therapy Designation Profitable Growth High confidence in multi-billion-dollar annual peak sales potential* Advances shift to wholly owned model Positions Genmab for sustainable long-term growth *Subject to results/regulatory approvals Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 4

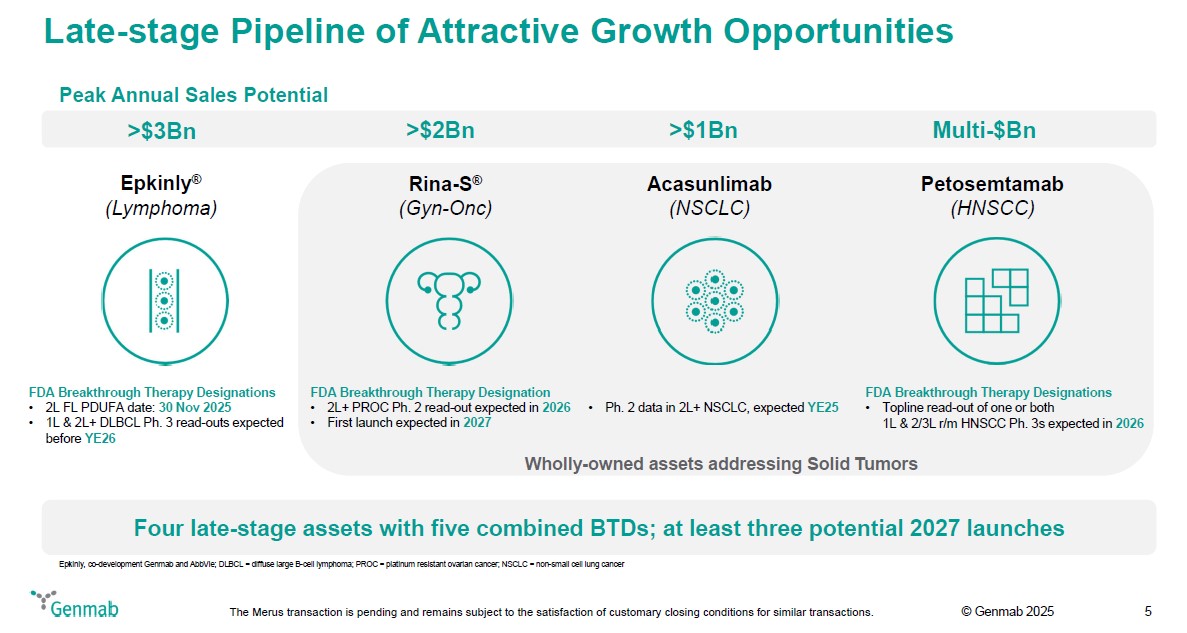

Late-stage Pipeline of Attractive Growth Opportunities Peak Annual Sales Potential >$3Bn Epkinly(R) (Lymphoma) FDA Breakthrough Therapy Designations 2L FL PDUFA date: 30 Nov 2025 1L & 2L+ DLBCL Ph. 3 read-outs expected before YE26 >$2Bn Rina-S(R) (Gyn-Onc) FDA Breakthrough Therapy Designation 2L+ PROC Ph. 2 read-out expected in 2026 First launch expected in 2027 >$1Bn Acasunlimab (NSCLC) Ph. 2 data in 2L+ NSCLC, expected YE25 Multi-$Bn Petosemtamab (HNSCC) FDA Breakthrough Therapy Designations Topline read-out of one or both 1L & 2/3L r/m HNSCC Ph. 3s expected in 2026 Wholly-owned assets addressing Solid Tumors Four late-stage assets with five combined BTDs; at least three potential 2027 launches Epkinly, co-development Genmab and AbbVie; DLBCL = diffuse large B-cell lymphoma; PROC = platinum resistant ovarian cancer; NSCLC = non-small cell lung cancer Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 5

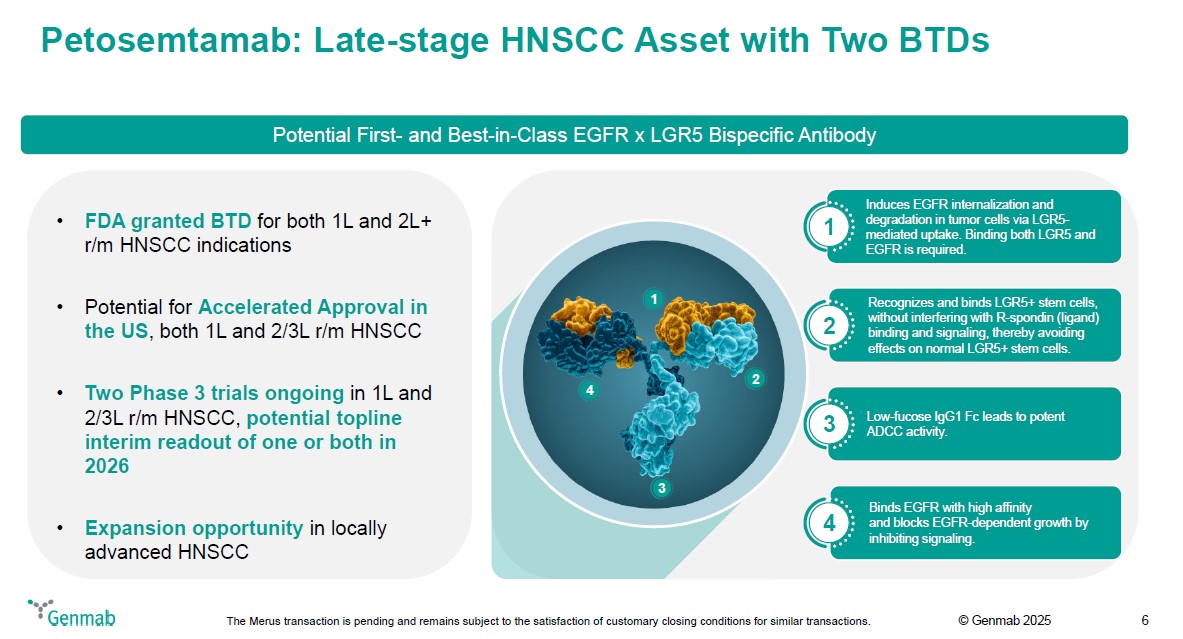

Petosemtamab: Late-stage HNSCC Asset with Two BTDs Potential First- and Best-in-Class EGFR x LGR5 Bispecific Antibody FDA granted BTD for both 1L and 2L+ r/m HNSCC indications Potential for Accelerated Approval in the US, both 1L and 2/3L r/m HNSCC Two Phase 3 trials ongoing in 1L and 2/3L r/m HNSCC, potential topline interim readout of one or both in 2026 Expansion opportunity in locally advanced HNSCC 1 2 3 4 1 Induces EGFR internalization and degradation in tumor cells via LGR5-mediated uptake. Binding both LGR5 and EGFR is required. 2 Recognizes and binds LGR5+ stem cells, without interfering with R-spondin (ligand) binding and signaling, thereby avoiding effects on normal LGR5+ stem cells. 3 Low-fucose IgG1 Fc leads to potent ADCC activity. 4 Binds EGFR with high affinity and blocks EGFR-dependent growth by inhibiting signaling. Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 6

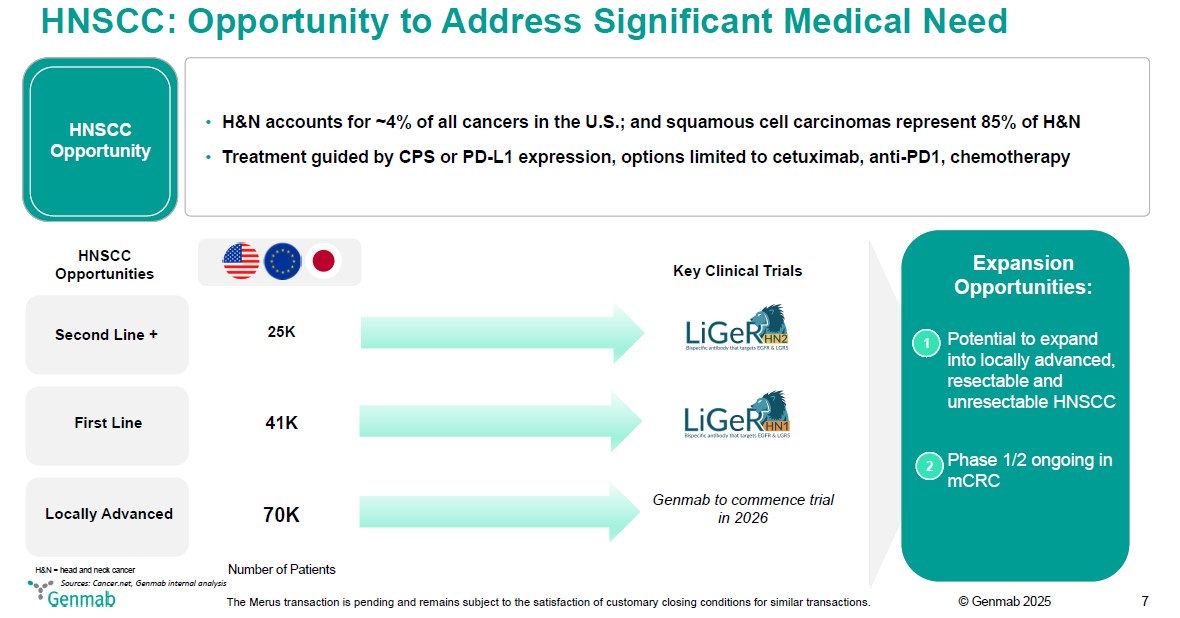

HNSCC: Opportunity to Address Significant Medical Need HNSCC Opportunity H&N accounts for ~4% of all cancers in the U.S.; and squamous cell carcinomas represent 85% of H&N Treatment guided by CPS or PD-L1 expression, options limited to cetuximab, anti-PD1, chemotherapy HNSCC Opportunities Key Clinical Trials Second Line + 25K LiGeR HN2 Bispecific antibody that targets EGFR & LGR5 First Line 41K LiGeR HN1 Bispecific antibody that targets EGFR & LGR5 Locally Advanced 70K Genmab to commence trial in 2026 H&N = head and neck cancer Number of Patients Expansion Opportunities: 1 Potential to expand into locally advanced, resectable and unresectable HNSCC 2 Phase 1/2 ongoing in mCRC Sources: Cancer.net, Genmab internal analysis Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 7

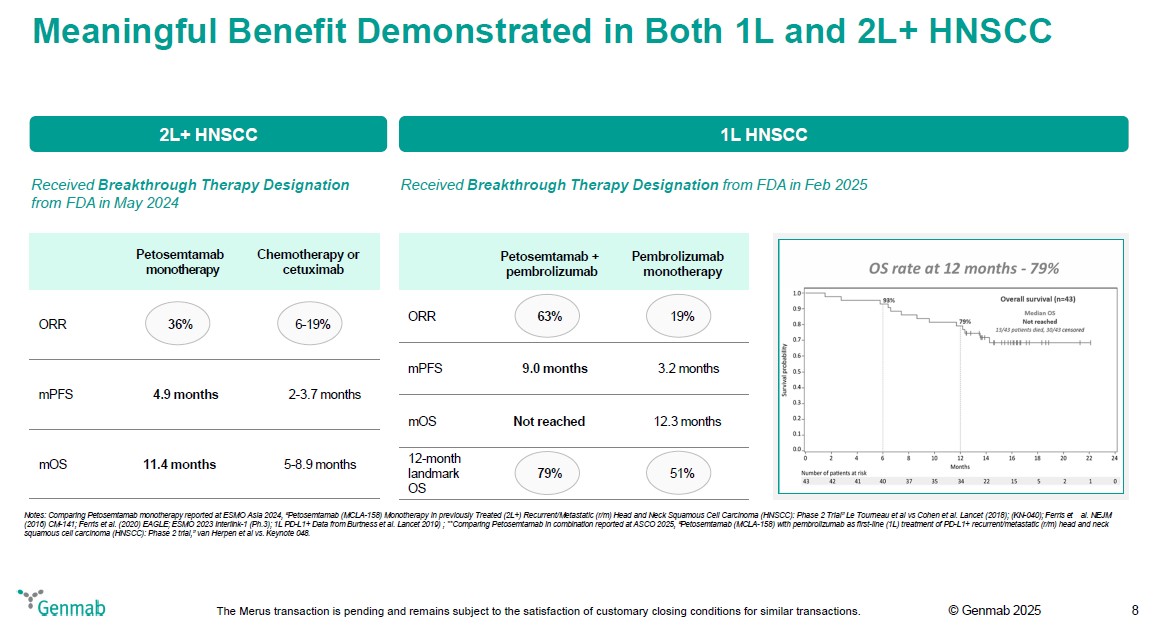

Meaningful Benefit Demonstrated in Both 1L and 2L+ HNSCC 2L+ HNSCC Received Breakthrough Therapy Designation from FDA in May 2024 Petosemtamab monotherapy Chemotherapy or cetuximab ORR 36% 6-19% mPFS 4.9 months 2-3.7 months mOS 11.4 months 5-8.9 months 1L HNSCC Received Breakthrough Therapy Designation from FDA in Feb 2025 Petosemtamab + pembrolizumab Pembrolizumab monotherapy ORR 63% 19% mPFS 9.0 months 3.2 months mOS Not reached 12.3 months 12-month landmark OS 79% 51% OS rate at 12 months - 79% Survival Probability 0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 Months 0 2 4 6 8 10 12 14 16 18 20 22 24 93% 79% Overall survival (n=43) Median OS 13/43 patients died, 30/43 censored Number of patients at risk 43 42 41 40 37 35 34 22 15 5 2 1 0 Notes: Comparing Petosemtamab monotherapy reported at ESMO Asia 2024, "Petosemtamab (MCLA-158) Monotherapy in previously Treated (2L+) Recurrent/Metastatic (r/m) Head and Neck Squamous Cell Carcinoma (HNSCC): Phase 2 Trial" Le Tourneau et al vs Cohen et al. Lancet (2018); (KN-040); Ferris et al. NEJM (2016) CM-141; Ferris et al. (2020) EAGLE; ESMO 2023 Interlink-1 (Ph.3); 1L PD-L1+ Data from Burtness et al. Lancet 2019) ; **Comparing Petosemtamab in combination reported at ASCO 2025, "Petosemtamab (MCLA-158) with pembrolizumab as first-line (1L) treatment of PD-L1+ recurrent/metastatic (r/m) head and neck squamous cell carcinoma (HNSCC): Phase 2 trial," van Herpen et al vs. Keynote 048. Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 8

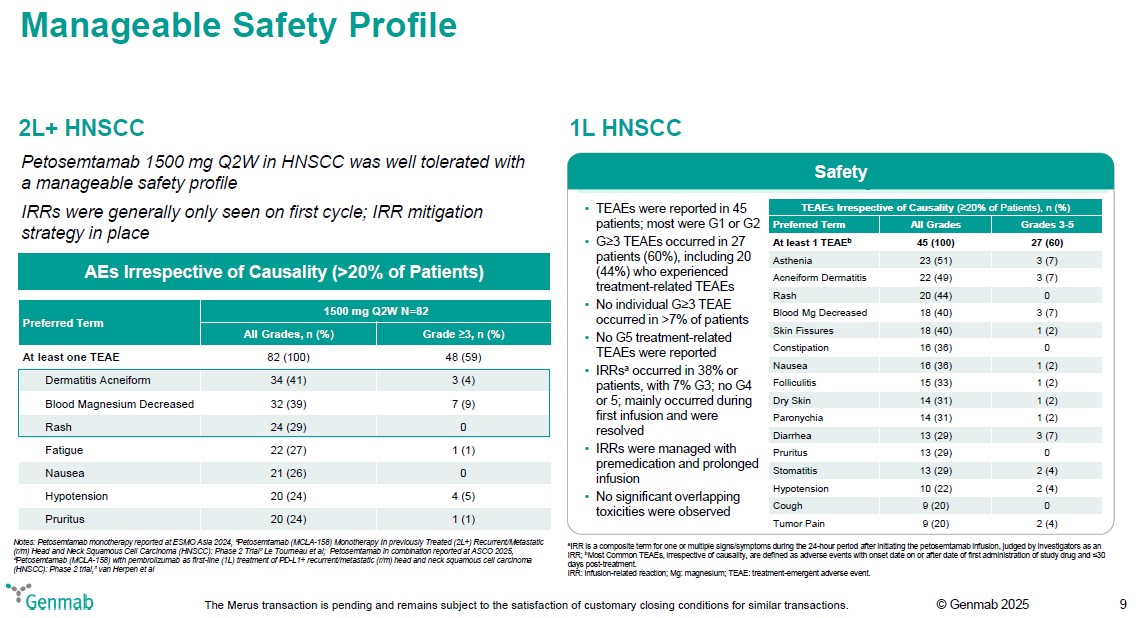

Manageable Safety Profile 2L+ HNSCC Petosemtamab 1500 mg Q2W in HNSCC was well tolerated with a manageable safety profile IRRs were generally only seen on first cycle; IRR mitigation strategy in place AEs Irrespective of Causality (>20% of Patients) Preferred Term 1500 mg Q2W N=82 All Grades, n (%) Grade (greater or equal)3, n (%) At least one TEAE 82 (100) 48 (59) Dermatitis Acneiform 34 (41) 3 (4) Blood Magnesium Decreased 32 (39) 7 (9) Rash 24 (29) 0 Fatigue 22 (27) 1 (1) Nausea 21 (26) 0 Hypotension 20 (24) 4 (5) Pruritus 20 (24) 1 (1) Notes: Petosemtamab monotherapy reported at ESMO Asia 2024, "Petosemtamab (MCLA-158) Monotherapy In previously Treated (2L+) Recurrent/Metastatic (r/m) Head and Neck Squamous Cell Carcinoma (HNSCC): Phase 2 Trial" Le Tourneau et al; Petosemtamab in combination reported at ASCO 2025, "Petosemtamab (MCLA-158) with pembrolizumab as first-line (1L) treatment of PD-L1+ recurrent/metastatic (r/m) head and neck squamous cell carcinoma (HNSCC): Phase 2 trial," van Herpen et al 1L HNSCC Safety TEAEs were reported in 45 patients; most were G1 or G2 G(greater or equal)3 TEAEs occurred in 27 patients (60%), including 20 (44%) who experienced treatment-related TEAEs No individual G(greater or equal)3 TEAE occurred in >7% of patients No G5 treatment-related TEAEs were reported IRRsa occurred in 38% or patients, with 7% G3; no G4 or 5; mainly occurred during first infusion and were resolved IRRs were managed with premedication and prolonged infusion No significant overlapping toxicities were observed TEAEs Irrespective of Causality ((greater or equal)20% of Patients), n (%) Preferred Term All Grades Grades 3-5 At least 1 TEAEb 45 (100) 27 (60) Asthenia 23 (51) 3 (7) Acneiform Dermatitis 22 (49) 3 (7) Rash 20 (44) 0 Blood Mg Decreased 18 (40) 3 (7) Skin Fissures 18 (40) 1 (2) Constipation 16 (36) 0 Nausea 16 (36) 1 (2) Folliculitis 15 (33) 1 (2) Dry Skin 14 (31) 1 (2) Paronychia 14 (31) 1 (2) Diarrhea 13 (29) 3 (7) Pruritus 13 (29) 0 Stomatitis 13 (29) 2 (4) Hypotension 10 (22) 2 (4) Cough 9 (20) 0 Tumor Pain 9 (20) 2 (4) aIRR is a composite term for one or multiple signs/symptoms during the 24-hour period after initiating the petosemtamab infusion, judged by investigators as an IRR; bMost Common TEAEs, irrespective of causality, are defined as adverse events with onset date on or after date of first administration of study drug and (less than or equal)30 days post-treatment. IRR: infusion-related reaction; Mg: magnesium; TEAE: treatment-emergent adverse event. Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 9

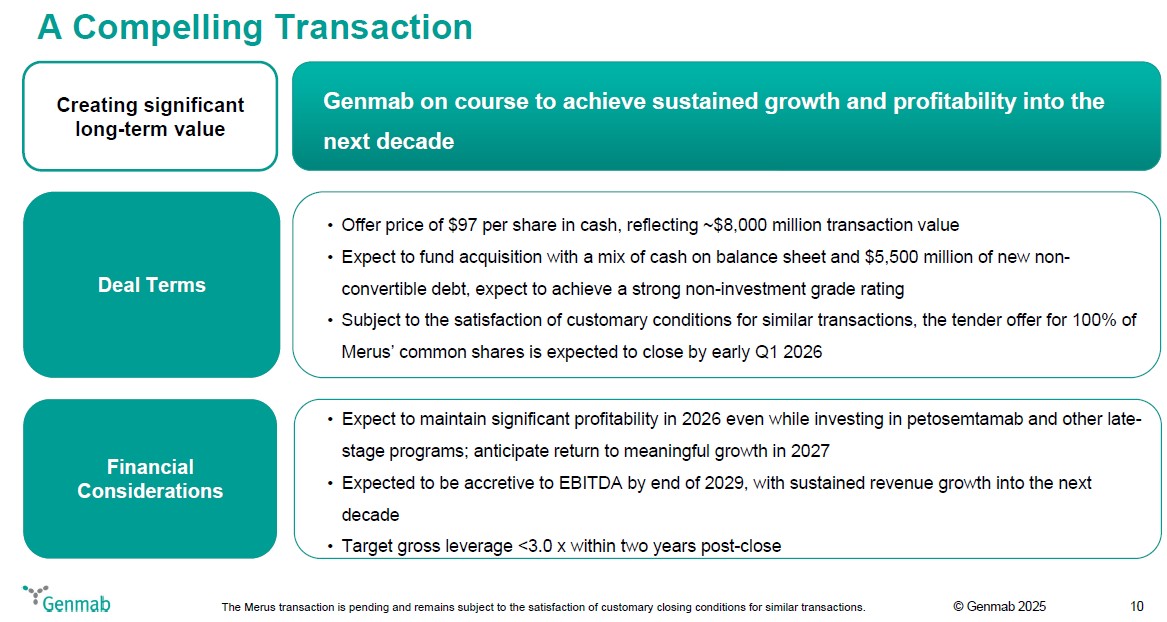

A Compelling Transaction Creating significant long-term value Genmab on course to achieve sustained growth and profitability into the next decade Deal Terms Offer price of $97 per share in cash, reflecting ~$8,000 million transaction value Expect to fund acquisition with a mix of cash on balance sheet and $5,500 million of new non-convertible debt, expect to achieve a strong non-investment grade rating Subject to the satisfaction of customary conditions for similar transactions, the tender offer for 100% of Merus' common shares is expected to close by early Q1 2026 Financial Considerations Expect to maintain significant profitability in 2026 even while investing in petosemtamab and other late-stage programs; anticipate return to meaningful growth in 2027 Expected to be accretive to EBITDA by end of 2029, with sustained revenue growth into the next decade Target gross leverage :lt;3.0 x within two years post-close Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 10

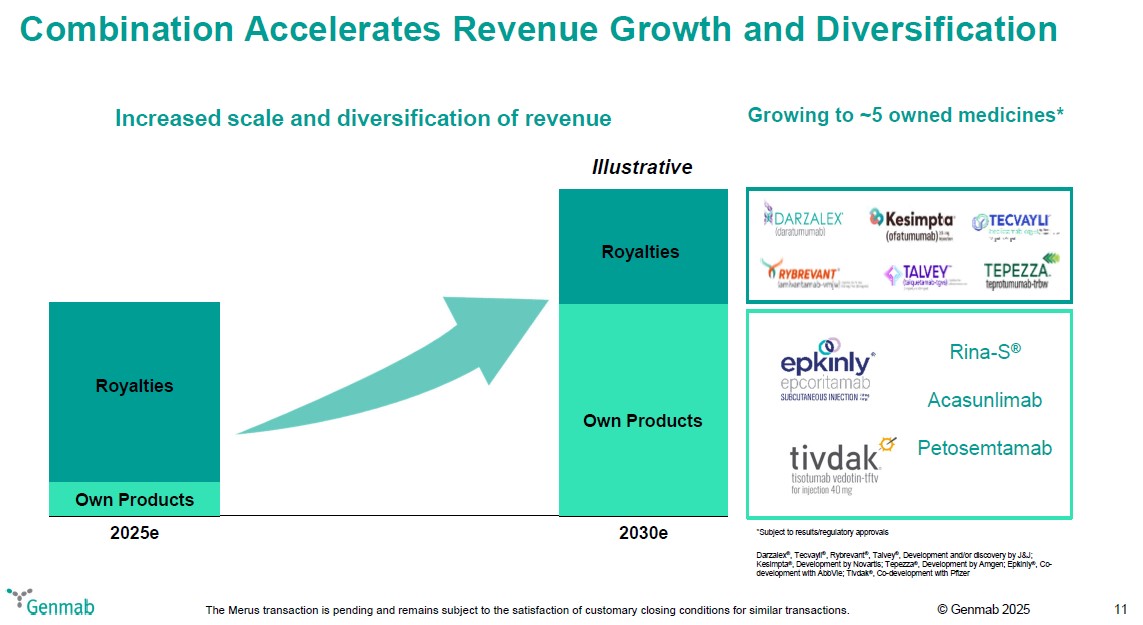

Combination Accelerates Revenue Growth and Diversification Increased scale and diversification of revenue 2025e Own Products Royalties 2030e Own Products Royalties Illustrative Growing to ~5 owned medicines* DARZALEX(R) (daratumumab) Kesimpta(R) (ofatumumab) 20 mg injection TECVAYLI(R) (teclistamab-cqyv) Injection for subcutaneous use 10 mg/mL and 90 mg/mL RYBREVANT(TM) (amivantamab-vmjw) Injection for IV Use 350mg/7mL (50 mg/mL) TALVEY(R) (talquetamab-tgvs) Injection for subcutaneous use 2 mg/mL and 40 mg/mL TEPEZZA(R) teprotumumab-trbw Epkinly(R) epcoritamab subcutaneous injection 48 mg 4mg Rina-S(R) Acasunlimab Tivdak(R) tisotumab vedotin-tftv for injection 40 mg Petosemtamab *Subject to results/regulatory approvals Darzalex(R), Tecvayli(R), Rybrevant(R), Talvey(R), Development and/or discovery by J&J; Kesimpta(R), Development by Novartis; Tepezza(R), Development by Amgen; Epkinly(R), Co-development with AbbVie; Tivdak(R), Co-development with Pfizer Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 11

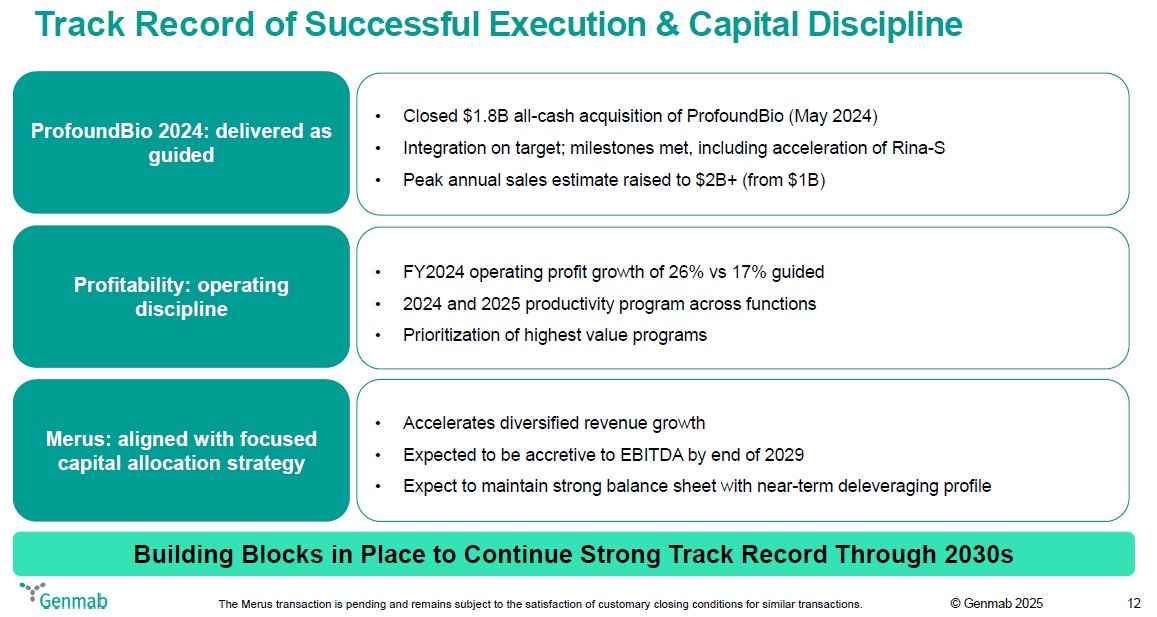

Track Record of Successful Execution & Capital Discipline ProfoundBio 2024: delivered as guided Closed $1.8B all-cash acquisition of ProfoundBio (May 2024) Integration on target; milestones met, including acceleration of Rina-S Peak annual sales estimate raised to $2B+ (from $1B) Profitability: operating discipline FY2024 operating profit growth of 26% vs 17% guided 2024 and 2025 productivity program across functions Prioritization of highest value programs Merus: aligned with focused capital allocation strategy Accelerates diversified revenue growth Expected to be accretive to EBITDA by end of 2029 Expect to maintain strong balance sheet with near-term deleveraging profile Building Blocks in Place to Continue Strong Track Record Through 2030s Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 12

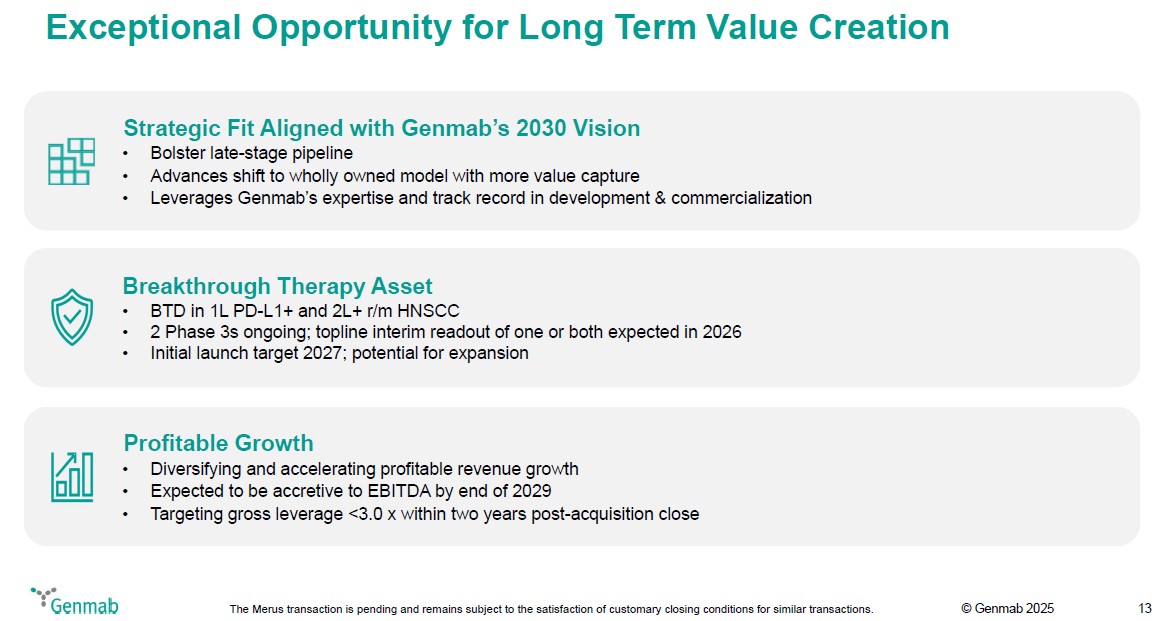

Exceptional Opportunity for Long Term Value Creation Strategic Fit Aligned with Genmab's 2030 Vision Bolster late-stage pipeline Advances shift to wholly owned model with more value capture Leverages Genmab's expertise and track record in development & commercialization Breakthrough Therapy Asset BTD in 1L PD-L1+ and 2L+ r/m HNSCC 2 Phase 3s ongoing; topline interim readout of one or both expected in 2026 Initial launch target 2027; potential for expansion Profitable Growth Diversifying and accelerating profitable revenue growth Expected to be accretive to EBITDA by end of 2029 Targeting gross leverage <3.0 x within two years post-acquisition close Genmab The Merus transaction is pending and remains subject to the satisfaction of customary closing conditions for similar transactions. (c) Genmab 2025 13

Q&A Genmab (c) Genmab 2025

Genmab 131,678 followers 8m #News Update: Genmab to acquire Merus, expanding our late-stage oncology pipeline and accelerating sustainable growth. Genmab has entered into an agreement to acquire Merus, a clinical-stage biotech with a breakthrough therapy in Phase 3 development for patients with advanced cancers. This proposed acquisition would diversify our promising late-stage pipeline and strengthen our foundation for sustainable growth. Fully aligned with our long-term strategy and track record in antibody innovation, it reinforces our commitment to accelerating therapies into the clinic and making a meaningful impact on patients. Learn more at: http://gmab.ly/N0Aa50X3pr8 #Oncology #Biotech Genmab News

Genmab @Genmab Breaking #News: Genmab to acquire Merus, a clinical-stage #biotech, expanding our late-stage #oncology pipeline and accelerating sustainable growth. This proposed acquisition aligns with our long-term strategy and track record in antibody innovation and strengthens our commitment to delivering innovative cancer therapies that can make a meaningful impact for patients. Learn more at: gmab.ly/M5Gv50X3pwl Genmab News

Jan van de Winkel, Ph.D. Following President and Chief Executive Officer at Genmab 1h Today, Genmab has entered into an agreement to acquire Merus, marking a pivotal moment for our company. I have always believed that a bold vision, combined with cutting-edge science and an unstoppable team is how we can make the greatest difference for patients. With decades of expertise in antibody medicines, we have grown thoughtfully and strengthened our capabilities strategically across research, development, and commercialization. This proposed acquisition reflects our commitment to becoming a fully integrated biotech company, delivering innovation from discovery all the way to patients. By adding Merus's late-stage oncology asset, a compelling strategic fit with our portfolio, we aim to build a stronger foundation for sustainable growth, expand our impact on patients by advancing new treatment options, and deliver long-term value for shareholders well into the next decade and beyond. http://gmab.ly/N0Aa50X3pr8 #Oncology #Biotech Genmab To Acquire Merus

Acquisition Of Merus By Genmab

Conference Call

Company Participants

| · | Anthony Pagano, Executive Vice President and Chief Financial Officer |

| · | Jan G. J. van de Winkel, Chief Executive Officer |

| · | Judith Klimovsky, Chief Development Officer |

| · | Judith V. Klimovsky, Executive VP & Chief Development Officer |

| · | Tahamtan Ahmadi, Chief Medical Officer |

Other Participants

| · | Asthika Goonewardene, Analyst, Truist Securities |

| · | Jonathan Chang, Analyst, LeeRink Partners |

| · | Judah Frommer, Analyst, Morgan Stanley |

| · | Matt Phipps, Analyst, William Blair |

| · | Michael Schmidt, Analyst, Guggenheim Securities, LLC |

| · | Qize Ding, Analyst, Redburn Atlantic. |

| · | Rajan Sharma, Analyst, Goldman Sachs International |

| · | TD Securities Participant |

Presentation

Operator |

Hello, and welcome to Genmab's Conference call regarding its proposed acquisition of Merus. As a reminder, this conference call is being recorded. During this telephone conference, you may be presented with forward-looking statements That include words such as believes, anticipates, plans, or expects. Actual results may differ materially, for example as a result of delayed or unsuccessful development projects. Genmab is not under any obligation to update statements regarding the future, nor to confirm such statements in relation to actual results, unless this is required by law. Please also note that Genmab may hold your personal data as indicated by you as part of our investor relations outreach activities in order to update you on Genmab going forward. Please refer to our website for more information on Genmab and our privacy policy. I would now like to hand the conference over to your first speaker today, Jan van der Winkel. Please go ahead.

Jan G. J. van de Winkel |

Hello and thank you for joining us today. We are sharing a transformative step for Genmab or planned acquisition of Merus. With me today to present this exciting news is our Chief Medical Officer Tahamtan Ahmadi, who will tell you about Merus exciting program petosemtamab or Peto, and our Chief Financial Officer Anthony Pagano who will walk you through the details of the proposed transaction.

For the Q&A we will be joined by Genmab's Chief Development Officer Judith Klimovsky and Chief Commercial Officer Brad Bailey. Before we continue, just a reminder, we will be making

forward looking statements so please keep that in mind as we go through the rest of this call, and here is some important information on where you will be able to read more about today's news.

The proposed acquisition of Merus marks a pivotal moment for our company. It clears Genmab's very high bar for innovation and aligns with our financial commitment of driving profitable and disciplined growth. Since the 2010s we have been successfully building an integrated biotech the Genmab way, having an impact on thousands of patients.

We are on track to achieve our 2030 vision and improve the lives of more patients with our wholly owned medicines. With this proposed acquisition, we will further strengthen our foundation as we add Peto to our already compelling late stage product pipeline. High potential assets like Peto, which have received two breakthrough therapy designations are truly unique and rare.

And our expertise and leadership in antibody based innovations as well as our rapid and broad clinical development of both EPKINLY and Rina-S are a testament to our ability to unlock Peto's full potential. We believe there is a clear path to market in multiple head and neck indications for Peto and we anticipate its initial launch could take place in 2027, and we are confident that Peto has multibillion dollar peak sales potential. The addition of revenue from Peto, once approved, will give us the flexibility to invest in the next winners from our innovative R&D pipeline. Genmab has delivered robust performance year over year. Our long term strategy has been to shift the company from a dependence on royalties into an end-to-end biotech, one that fully owns, develops and commercializes our own Medicines. Peto provides us with a unique opportunity to both advance that shift to a 100% owned model and maximize our long term growth altogether. Genmab is on course to achieve sustainable growth and profitability into the next decades and beyond. Here you can see how the addition of Peto change enhances our late stage pipeline. These programs represent the future of Genmab. We will have three products with five breakthrough therapy designations between them. That means that the FDA believes each of these therapies has the potential to substantially improve outcomes for patients over existing therapies. Importantly, Rina-S, acasunlimab and Peto would be 100% owned assets, positioning Genmab as an antibody focused biotech powerhouse and together with EPKINLY they underpin our sustainable long term growth. We are confident in our late stage pipeline and excitingly we anticipate a number of significant catalysts in the next 12 to 24 months. As Merus has stated, we expect top line interim readout of one or both of the Phase 3 Peto trials in 2026 for EPKINLY. We are anticipating the potential approval in second line follicular lymphoma in November and in 2026 we expect data in frontline diffuse large B cell lymphoma. Also, next year we expect potentially registrational data in platinum resistant ovarian cancer for Rina-S and following these significant readouts we anticipate critical launches and indication expansions across EPKINLY, Rina-S and Peto in 2027. So, with this exciting news I will ask Tai to provide you with the details of why we are so very enthusiastic about battle. Tai, the floor is yours.

Tahamtan Ahmadi |

Thank you Jan. Similar to EPKINLY and Rina-S, we view Peto as one of these truly rare assets that are a pipeline within a product. But to start with the basics, Peto is an EGFRxLGR5 bispecific antibody with the potential to become the first and best in class therapy for head and neck. We've seen meaningful clinical benefit in both first and later line head and neck cancer settings and this has been recognized by the FDA which granted breakthrough therapy designation for both the first line PDR1 positive and second line plus recurrent or metastatic head and neck cancer. There are two Phase 3 trials ongoing, one in first line and one in second line head and neck. And as Jan just noted, we anticipate potential top line data for one or both of these trials already in 2026 and as Merus has publicly indicated, there is a clear path for accelerated approval under Project Frontrunner agreed with the FDA in both indications. Importantly, as we have been doing with Rina-S, and are doing with Rina-S, there are multiple significant opportunities for expansion beyond the ongoing Phase 3 trials.

There remains a significant need for innovative treatments in head and neck cancer with current standard of care delivering modest progression free survival and overall survival in frontline disease. An active and well tolerated bispecific could materially change outcomes for patients. In addition to first and second line, Peto's emerging profile supports a strategy to expand development into locally advanced head and neck cancer. So, this is our first planned next step with our goal to initiate the first phase trial in this indication in 2026 and we will provide you with more specific details in terms of both timing and trial design next year. So now let's take a look at some of the data behind our confidence and our enthusiasm for Peto. The data to date are highly compelling in both first line head and neck in combination with standard of care and in second line plus head and neck. As a single agent, Peto has demonstrated a meaningful clinical benefit. In the second and third line setting, standard of care typically achieves objective response rates around 6% to 19%. By contrast, Peto demonstrated a 36% response rate with improvement also observed in both progression free survival and overall survival. Equally, the data in the first line setting are also highly encouraging. Peto here in combination with Pembro achieved a 63% response rate that is more than three times higher than the 19% that have been observed with the standard of care. And again, this benefit is not limited to response rate, but it's also reflected in improvements in event-driven endpoints such as progression, free survival and overall survival. It is this data on which the FDA based its granting of two PDD breakthrough designations for Peto. This recognition underscores our confidence in Peto's potential to meaningfully improve outcomes for patients with head and neck. Importantly, these results support moving the combination into earlier setting locally advanced disease where the treatment opportunity and medical need is even greater. Now turning to safety. In addition to its efficacy, Peto has been shown to be well tolerated with a manageable safety profile. Infusion related reactions were generally confined to the first cycle with a mitigation plan in place and overall the risk benefit supports advancement across lines and combination. So, in summary, we believe that our expertise in both clinical development and commercial execution will allow us to maximize the potential of Peto, giving us another opportunity to rapidly advance innovation into the clinic and automate it to patients and I would now like to hand it over to Anthony to take you to the financial details of this transaction. Anthony.

Anthony Pagano |

Thanks Tai. I'd like to begin by reiterating how enthusiastic we are about Merus and what this acquisition means for the future of Genmab. This proposed transaction will have a substantial and positive impact on Genmab's growth trajectory. Under the terms of the transaction, Genmab will acquire Merus at an offer price of $97 per share in cash, which equates to around $8 billion.

We will fund the transaction with a mix of existing cash and new debt and we expect to achieve a strong non-investment grade rating. We anticipate that the transaction will close by early in the first quarter of 2026 subject to the receipt of regulatory clearances. Now I'd like to take a moment to frame the financial considerations.

We are confident that Peto has the potential to meaningfully improve outcomes for patients with head and neck cancer, but in order to unlock this potential will need to invest. So, as you'd expect, there will be a step up over the near to medium term in R&D and commercialization expenses as we invest in Peto as well as our existing late stage programs. Even with this investment, we will maintain significant profitability in 2026 and we'll expect Meaningful growth in 2027 as launch revenues build and our spending normalizes, we anticipate we will be approaching break even on the transaction in 2028 and the transaction will be accretive to EBITDA a year later as we believe Peto has the potential to reach at least $1 billion in revenue by 2029. Further, we are committed to rapidly deleveraging and a robust financial foundation will allow us to pay down this debt significantly within two years after the closing of the proposed transaction, giving us low leverage by the end of the decade.

So, we are planning for sustained growth and profitability into the next decade as we unlock meaningful value from our late stage assets and maximize the potential of our commercialized medicines. Now I want to take a moment to look more closely at just how the addition of Peto to our pipeline will help us achieve this sustained growth. Adding Peto to our portfolio not only increases our scale, it significantly advances our strategy to reduce dependence on royalties by diversifying our sources of revenue which will address our path to growth and profitability by the end of the decade and beyond. As you can appreciate, there are essentially two parts of our business. We have the royalty products which include six out licensed therapies and then we have our co owned and wholly owned assets. Let's remember, in addition to DARZALEX, we also have five other royalty products with the potential for more to come and all of which have significant potential for growth into the next decade. Together these will continue to serve as a solid foundation of recurring revenue for Genmab well into the future. But what's really exciting for us at Genmab is the potential of our proprietary products. These are the promising late stage programs that we are investing in today that provide us with significant growth prospects moving forward. We believe that the data we are anticipating next year will serve as proof points for our conviction that EPKINLY, Rina-S and now Peto all have multibillion dollar potential. In summary, we have multiple streams of growing recurring revenue. These have laid the groundwork for our success and now with the addition of Peto to our high potential late stage portfolio, we will be well positioned to move into Genmab's next phase of growth Our confidence in our projected growth comes from our track record. We have proven that we are excellent evaluators of innovation and that we can deliver on our promises. We over delivered on our financial commitments made at the time of the Profound Bio acquisition and we rapidly accelerated the development of Rina-S. We had roughly 40 patients worth of data when we acquired Profound Bio. And we're going to exit this year with three ongoing Phase 3 trials and two potentially registrational Phase 2s for Rina-S. We have also proven that we are disciplined in our execution against our capital allocation framework and prioritization of our investments. And we continue to be committed to delivering profitable growth. The addition of Peto will be absolutely key to achieving this. So, in summary, our differentiated approach to building a fully integrated biotech company started in the 2010s has continued here into the 2020s and now we have high conviction that we have the building blocks in place to continue this strong track record through the 2030s. The proposed acquisition of Merus and the addition of Peto to our pipeline is firmly on strategy and has the potential to bring another breakthrough therapy to patients and help drive long term sustainable growth for Genmab. So, with that I'm going to hand you back over to Jan.

Jan G. J. van de Winkel |

Thank you Anthony. So let me summarize. The proposed acquisition of Genmab is an exceptional opportunity that advances our evolution into a global biotech leader. It accelerates our shift towards a 100% owned model. It expands and diversifies our revenue and it brings us closer to achieving our 2030 vision to improve the lives of patients.

The first Peto launch is anticipated in 2027 with real potential for it to join EPKINLY and Rina-S as multi billion dollar program. Combined with a disciplined capital allocation, strong financial foundation and proven commercial execution, this transaction sets us up for durable long term growth into the next decade. We are pleased to answer any questions you may have. So, I will now turn the call back to the operator and open the call for questions.

Questions And Answers

Operator |

Thank you. (Operator Instructions) Please note there is a limit of one question per person on today's call. We'll now move on to our first question. Our first question comes from the line of Jonathan Chang from LeeRink. Please go ahead, your line is open.

Q - Jonathan Chang

Good morning. Congrats on the proposed acquisition and thanks for taking my question. How much does the CRC opportunity contribute to your decision and price of the acquisition? And when could we see data on CRC and what could we see in that update? Thank you. |

A - Jan G. J. van de Winkel

Thanks, Jonathan, for that question. I think I will take this one myself. CRC data will come in the coming months and will be released by Merus. And we have based our whole model only on the head and neck cancer data.

Q - Jonathan Chang

Got it. Thank you. |

A - Jan G. J. van de Winkel

Thank you, Jonathan.

Operator |

Thank you. We'll now move on to our next question. Our next question comes from the line of Michael Schmidt from Guggenheim Partners. Please go ahead. Your line is open.

Q - Michael Schmidt

Hey, good morning and thanks for taking my questions and congrats for me as well on the proposed deal. Could you talk a bit about the timing of the acquisition? You're obviously taking on some clinical risk and talk about your comfort level in stepping in with the proposed deal prior to the Phase 3 data reading out next year. And then I also had a question on the investment that may be necessary to maximize the potential of petosemtamab globally. Can you talk about that as well? Thank you so much. |

A - Jan G. J. van de Winkel

Thank you, Michael, for the question. I will take the first one and then Anthony can take the second one. We think that the timing is perfect here. We have done very deep due diligence and, and we understand Peto really, really well, Michael. So, we have, I think, went through 56,000 files, I think, in due diligence. And we are very, very confident that this is a potential game changing, potentially transformational bispecific antibody. We understand bispecifics really well, as well as head and neck cancer.

Remember that we had a number of programs active at TIVDAK and also with GEN1042 in head and neck. So, we could really value the strength of the data, I think better than other companies potentially can do. And we believe that this is perfect timing for us to actually first approach Merus and now come to an agreement with them because it will be the exact building block we need to very convincingly grow into a profit into the next decades together with molecules like Rina-S, EPKINLY and acasunlimab. So, we think the timing is just perfect. The confidence level is super high. I want to leave it with that and then hand it over to Anthony to maybe talk a bit more about the investment levels needed to optimally and broadly maximize the potential for Peto.

A - Anthony Pagano

Yeah, thanks Michael. I mean, as a starting point, if we think about the opportunity for Peto from my perspective, to very clearly clears our high bar for innovation. At the same time, Michael clears that high bar we have here at Genmab for investment. Now moving forward, you're going to see the same focus and disciplined approach to how we run this business and how we invest back into our business.

Further, Peto in this overall deal is fully in line with our capital allocation framework. And Peto again is that opportunity, that potential breakthrough therapy asset where we want to prioritize investment and that's fully in line with our capital allocation framework. Again, this is a late stage program with important data readouts in 2026 and has the potential to launch again in 2027.

So absolutely we will be investing accordingly. We will resource Peto to unlock its full potential both from an R&D and commercialization perspective. From a commercialization perspective, we have a very strong foundation that we built out here, particularly in the United States and Japan and we'll be looking to leverage that investment. And as you know, we've started to build out in Europe. So, we feel very comfortable that we have a very strong foundation that we can leverage. At the same time, Michael, we're not going to shy away from making the necessary investments.

Just very quickly then reiterate what I covered in my prepared remarks as we get into 2026. Again, we fully expect to retain significant profitability in 2026, have meaningful growth in 2027 and we expect this transaction to be approaching break even in 2028 and to be accretive in 2029. So overall we really like the setup here from an overall financial profile perspective, as a reminder again, we not only delivered but over delivered on the financial commitments we made to the market the last time we did an acquisition and acquired Rina-S from Profound Bio. So overall, Michael, you should expect the same focus and discipline approach from the Genmab management team here.

A - Jan G. J. van de Winkel

Thank you, Anthony. Let's hand back to the operator.

Operator |

Thank you. We'll now move to our next question. Our next question comes from the line of Asthika Goonewardene from Truist. Please go ahead. Your line is open.

Q - Asthika Goonewardene

Hi, good morning guys. Thanks for taking my questions and congrats on the deal. So, it's good to see that you already have plans to commence the trial in locally advanced head and neck cancer. But to Jonathan's question earlier, you could potentially see some sufficient data in colorectal cancer expansion cohorts that might illustrate a potential path to marketing CRC as well in the near term. So, I just want to get an idea from you. How would you prioritize that? If you do see a signal in CRC, how would you prioritize that versus expanding to locally advanced head and neck? And then if I can just tag |

Q - Michael Schmidt

On something extra here, just want to get your comments on what you think about the LGR5 mechanism of action specifically relating to head and neck and colorectal. Which one makes more sense to you? Thanks. |

A - Jan G. J. van de Winkel

Thanks, Asthika, for the question. Why don't we ask Tai to first give you perspective on the prioritization of colorectal versus locally advanced head and neck and then also talk a bit about the mechanism of action of Peto. This is what you refer to. And then let me see whether Judith can then add to that. Tah, why don't you start?

A - Tahamtan Ahmadi

Yeah, thank you, Asthika for the question. And I would start with what is in the public data and this is of course what we at this point can talk with confidence in the public space is the head and neck data. We've obviously done a lot of diligence on all the data that Merus has, but the focus right now is to talk about our plants in head and neck. Merus did a fantastic job in starting a very broad focus development with two Phase 3s that will read out in '26. And this is the area where you have a signal in the public domain single agent activity, good combinability, good safety profile with high response rates that then allows us to talk about the first of many plants which is to move into the local regional space. I think it's premature for us to have a conversation about colorectals until Merus has publicly released the data.

And at that point we would be very happy to discuss what our thoughts that we of course have on colorectals are as it relates to the mechanism of action of the asset, I think Merus itself spoke about that, they are looking into trying to further elucidate the biology, but broadly speaking, what it does disintegrates and basically binds to EGFR, internalizes it. Don't really see a reason why it would play out differently in one EGFR positive disease over the other. Haven't seen any reasons to believe that. We like the profile, we like the potential of the drug and we're really excited and as we said in the beginning, we view this as a potential pipeline within a drug. Thank you.

A - Jan G. J. van de Winkel

Thanks, Tai. Judith, do you want to add anything to that?

Yeah, only two things that there are strong preclinical data on different models of organoids to support LGR5 in different settings, among them colorectal. And I want to echo Anthony on our commitment to unleash the full value of Peto as data provide signals to your question on potential prioritization that's it. Thanks. Thanks, Judith. Let me hand it back to the operator and see whether there are any additional questions. Thanks, Asthika.

Operator |

Thank you. Would you Now move on to the next question. Our next question comes from the line of Judah Frommer from Morgan Stanley. Please go ahead. Your line is open.

Q - Judah Frommer

Hi. Thank you. Congrats on the announcement and thanks for taking the question. Maybe just one on your assumptions around peak market share potential and head and neck. First line, specifically, can you share with us any thoughts around peak market share in HPV positive versus HPV negative head and neck and the competitive landscape within those two subsets? Thank you. |

A - Jan G. J. van de Winkel

Thanks Judah for the questions. Anthony, why don't you give this a go and then I can ask Tai to add to that.

A - Anthony Pagano